Hybrid Long Term Care Insurance

Discover how hybrid long term care plans combine life insurance protection with comprehensive long term care coverage — ensuring your premiums never go to waste.

Death Benefit Guarantee

If you never need long term care, your beneficiaries receive a tax-free death benefit.

Stable Premiums

Unlike traditional LTC insurance, hybrid plans offer guaranteed premiums that won't increase.

Flexible Coverage

Customize your coverage with various benefit periods, inflation protection, and care options.

Why Choose Hybrid Long Term Care Insurance?

Hybrid policies combine the best of life insurance and long term care coverage, ensuring your investment provides value no matter what happens.

Asset Protection

Protect your retirement savings and assets from the devastating costs of long term care, which can exceed $100,000 annually.

Comprehensive Care Coverage

Coverage for nursing homes, assisted living, memory care, home health care, and adult day care services.

Return of Premium

Many hybrid policies offer a return of premium option if you decide to cancel your coverage or no longer need it.

Guaranteed Premiums

Lock in your premiums at purchase — they're guaranteed never to increase, unlike traditional LTC insurance.

Spousal Benefits

Shared care options allow couples to share a pool of benefits, providing flexibility and potential cost savings.

Tax Advantages

Qualified hybrid LTC policies offer tax-free benefits when used for long term care expenses.

How to Get Started

Finding the right hybrid long term care plan is easier than you think. Here's how the process works.

Assess Your Needs

Determine how much coverage you need based on your age, health, assets, and family situation.

Compare Options

Review policies from multiple carriers to find the right balance of coverage, features, and cost.

Apply & Qualify

Complete the application process with underwriting that considers your health and medical history.

Enjoy Peace of Mind

Rest easy knowing your care is covered and your assets are protected for you and your family.

Top Hybrid LTC Insurance Companies

We work with the most reputable insurance carriers to find the best coverage for your needs.

Lincoln Financial

Industry leader in hybrid LTC with flexible premium options and strong financial ratings.

Nationwide

Offers both life insurance and annuity-based hybrid products with innovative features.

Pacific Life

Known for competitive pricing and comprehensive coverage options for individuals and couples.

OneAmerica

Specializes in annuity-based hybrid products, ideal for repositioning existing assets.

What Our Clients Say

Hear from real people who have secured their futures with hybrid long term care insurance.

"After my mother needed care, I saw firsthand how expensive it can be. My hybrid policy gives me peace of mind knowing I'm protected without losing my premiums if I never need care."

"The guaranteed premiums were a game-changer for me. I couldn't risk my rates increasing every few years like with traditional LTC insurance."

"Our advisor helped us find a shared care policy that works perfectly for my wife and me. We have flexibility and comprehensive coverage at a reasonable cost."

LTC Coverage Is More of a Necessity Than an Option

The United States population is aging as baby boomers reach retirement. By 2040, Americans age 65+ will nearly double to approximately 80 million. The fastest-growing segment — those aged 85+ — will nearly quadruple. These demographic shifts have driven long-term care costs upward significantly.

| Service Type | 2025 Annual Cost | 2030 Projected Cost |

|---|---|---|

| Homemaker Services | $68,640 | $83,867 |

| Home Health Aide | $74,256 | $85,999 |

| Adult Day Care | $28,677 | $35,765 |

| Assisted Living Facility | $70,800 | $84,001 |

| Nursing Home (Private Room) | $120,840 | $144,297 |

Paying for Long Term Care: What Are the Options?

Most people purchase long-term care plans to shield assets from extraordinary care expenses, which can easily reach hundreds of thousands annually. High-net-worth individuals may self-insure for long-term care. We recommend self-insurance only for those with assets exceeding $2 million.

Long-term care needs can extend five years or longer. Consider worst-case scenarios and how self-insurance affects your retirement finances and legacy planning.

Traditional LTC Insurance

Traditional LTC insurance, popular since the 1980s, operates similarly to health, homeowner, and auto insurance. Premiums use a “pay-as-you-go” structure and carry no cash value — unused premiums are forfeited if long-term care services aren't required. Many existing traditional policies experienced unpredictable premium increases, reducing their appeal. Annual policy sales declined dramatically: from approximately 750,000 in the early 2000s to fewer than 60,000 in 2018.

Annuity-Based Long-Term Care

Fixed or indexed annuities can offset long-term care expenses. If long-term care is needed, monthly benefits double or increase. Many LTC hybrid annuity products don't require health qualification if applicants lack an Alzheimer's diagnosis or nursing home residency. While annuities address coverage, they're less attractive from a benefit perspective. We recommend annuities primarily for those with serious health issues preventing qualification for hybrid long-term care insurance.

Hybrid Long-Term Care Plans

Hybrid long-term care plans combine life insurance with long-term care riders. Policies pay death benefits upon policyholder death, like standard life insurance. Additionally, if the insured requires long-term care while living, the policy functions like traditional LTC insurance. People aged 50 to mid-60s typically invest $70,000 to $150,000 per person for hybrid plans offering benefits comparable to traditional LTC coverage. Hybrid companies allow single-premium or ten-year payment options, with no further premiums required.

Hybrid vs. Traditional Long-Term Care Insurance

Understanding the key differences helps you choose the right product for your situation.

Premium Structure

Annual premiums subject to unpredictable increases

Fixed premiums guaranteed never to increase — lump sum or spread over up to 10 years

If Care Not Needed

All premiums forfeited — use it or lose it

Tax-free death benefit paid to your beneficiaries

Medical Qualification

Stricter underwriting; many applicants declined

Easier to qualify — companies accept more significant health issues

Tax Advantages

Limited tax benefits

Tax-free 1035 exchanges from existing annuities or life insurance; tax-free death benefit

Hybrid Life Insurance Policies Are Increasingly Popular

The past several years have witnessed tremendous growth in hybrid LTC sales, driven by guaranteed premiums and full-premium return with interest at death.

“In the past 36 months we have seen a 520% increase in buyers of hybrid long-term-care insurance. Buyers are opting for hybrid LTC insurance plans in the place of traditional plans 5 to 1. They are also choosing hybrid plans for the premium stability and tax-free death benefit.”

Jim Roberts, LTC Specialist

Senior specialist at hybridlongtermcareplans.com • Marketing traditional long-term care insurance across all 50 states since 1998

Types of Hybrid Life Insurance Products

Hybrid long-term care plans derive from permanent life insurance and are classified into three types by structure.

Linked-In Hybrids

The most common type — combines LTC insurance with life insurance or annuities. Provides a money pool paying long-term care expenses when needed, or returning death benefits or annuity cash value.

Sample Policy

A 60-year-old married woman contributes $90,000 single-premium, generating a $154,000 death benefit and $463,000 in LTC benefits — $6,429/month for a 6-year benefit period.

Life Insurance with LTC Rider

Primarily life insurance with an LTC accelerated death benefit option. When long-term care is needed, death benefits or portions thereof become available, typically paying monthly as a death-benefit percentage.

Sample Policy

$200,000 death benefit with 3% LTC rider provides $6,000/month in LTC benefits for 33 months. With an 80% acceleration clause, ~$4,800/month with $40,000 remaining death benefit.

Critical Illness Riders

Critical illness features accelerate death benefits when policyholders become chronically ill long-term. These pay lump sums when diagnosed with specified conditions like heart attack, stroke, or cancer.

Sample Policy

$200,000 death benefit with 70% chronic illness acceleration provides up to $140,000 in benefits at $2,800/month.

Tax Advantages of Hybrid Policies

Long-term care expenses reduce the death benefit. The remaining death benefit awarded to beneficiaries isn't subject to taxation. This proves advantageous versus retirement account assets like traditional IRAs, 401(k)s, and 403(b)s, which are taxed when transferred to non-spouse beneficiaries.

Cost of Coverage

Hybrid LTC is typically more expensive than traditional long-term care — understandably, since it combines life insurance benefits with long-term care coverage. Premiums are often paid as single payments but can spread across time periods (typically under 10 years). Unlike traditional LTC with unpredictable premium increases, hybrid policy payments remain fixed.

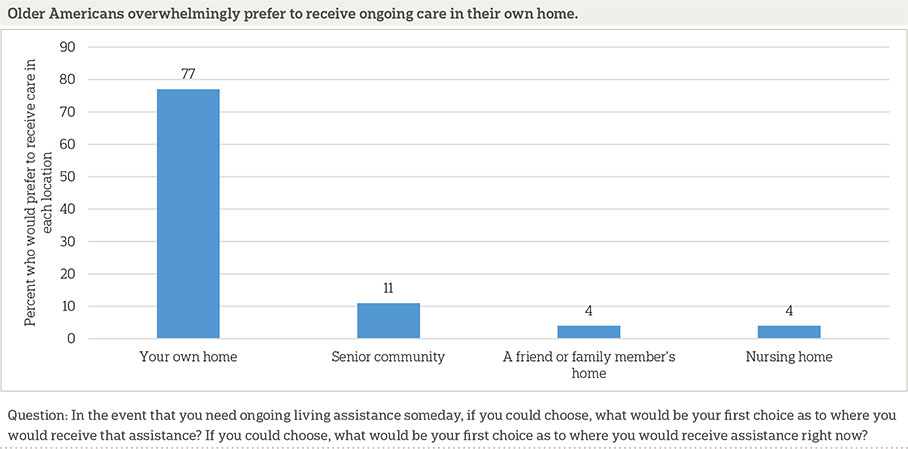

Which Care Facilities Do Americans Prefer?

According to the Associated Press NORC long-term care poll, the majority (77%) of Americans prefer receiving care at home.

- 77% prefer care at home

- 11% prefer a senior community

- 4% prefer a family member's home

- 4% prefer a nursing home

Medicare & Medicaid for Long Term Care

Medicare — Does It Help?

Medicare covers some long-term care services but provides very limited assistance and cannot be relied upon. Medicare specifically doesn't cover long-term care or custodial care — activities of daily living assistance like eating and dressing — which constitute significant nursing home, assisted living, and other LTC facility services. Coverage is limited to 100 days of skilled nursing care per illness.

Medicaid — Does It Help?

Unlike federally-operated Medicare, Medicaid is state-administered with varying long-term care coverage. Eligibility requires inability to perform at least two of six activities of daily living and near-complete income and asset depletion. States maintain a 5-year look-back period. Medicaid should never be a first choice for long-term care coverage.

| Criteria | Medicare / Medicaid | Long-Term Care Insurance |

|---|---|---|

| Availability | Generally 65+ or younger with permanent disabilities; Medicaid requires asset depletion | Purchasable at any age; cheapest between late 40s and late 50s |

| Eligibility | Medicare: 3+ day hospital stay, certified facility within 30 days; Medicaid: income/asset limits | Unable to perform 2+ of 6 ADLs or having dementia/cognitive impairment |

| Coverage | Medicare: up to 100 days skilled nursing; Medicaid: nursing home from day one but limited facility choice | Extensive home care, assisted living, nursing home; full freedom choosing facilities; 1-year to unlimited periods |

How to Buy a Hybrid Policy

Hybrid LTC premiums range from $50,000 to $100,000, typically paid as single lump sums. Policyholders unable or unwilling to pay lump sums may spread premiums over time (e.g., 5 years, 7 years). In certain cases, policyholders can add LTC riders to existing life insurance or exchange existing life policies for life-LTC hybrids at reasonable costs.

Age Flexibility

Hybrid policies are purchasable at any age. Premiums are cheapest when younger and in good health, but most people purchase this protection after age 60. Some companies issue policies to Americans up to age 85.

Underwriting Process

The process includes a health questionnaire, phone or face-to-face interviews, and medical records review. Hybrid policy underwriting is typically less complicated than traditional LTC insurance, enabling most applicants to qualify easily.

Testimonials From Our Readers

“We saw three different brokers before Patricia suggested we look online. This site presented an online form that we completed in 5 minutes. About a week later, we received a green binder enclosing policies from almost all major LTC insurers in the country. We compared the policy terms and made up our minds within 24 hours.”

“Buying LTC coverage is something I have always had in mind since I had a major health incident in 2015. Everything became much easier when I learnt about hybrid coverage that preserved my contributions if long term care won't be needed. Hybrid Long Term Care Plans made it super easy to find the right policy aligned with my retirement plans!”

Frequently Asked Questions

What is a hybrid policy?

A hybrid life policy combines life insurance and long-term care insurance. By default, the policy accumulates death benefits paid to beneficiaries upon policyholder death. If long-term care is needed during the policyholder's lifetime, the death benefit accelerates to offset expenses. Remaining amounts after long-term care expenses are paid remain as death benefits to appointed beneficiaries. This dual-insurance approach guarantees the insured won't lose premiums whether or not long-term care is needed.

Which is better — traditional LTC insurance or hybrid life-LTC combos?

Both products have unique characteristics suiting different policyholders. Newer hybrid life/LTC combos offer distinct advantages: they carry death benefits if long-term care isn't needed and usually include cash-value components. Conventional long-term care plans forfeit all premiums if long-term care services aren't required. Traditional plans are cheaper and provide larger benefits. Most contemporary policyholders prefer hybrid combos, though traditional plans may suit some circumstances.

Which is cheaper — traditional LTC or hybrid LTC?

Hybrid LTC life insurance is generally more expensive than traditional long-term care coverage. Premiums are paid as single lump sums or spread across years (typically under 10 years). While hybrid LTC costs more, these policies avoid the rampant premium increases affecting traditional long-term care insurance.

What do beneficiaries get if LTC insurance isn't used?

If long-term care becomes unnecessary, the policy functions like conventional life insurance with death benefits paid to appointed beneficiaries. If long-term care is needed during your lifetime, the policy allows accelerating (drawing down) the death benefit for those services. Remaining amounts are still given to beneficiaries.

Is hybrid long-term care insurance worth it?

14 million American adults required long-term care services in 2018. Medicaid assists with custodial care but only after near-complete asset depletion. Hybrid LTC policies specially combine life insurance with LTC benefits so beneficiaries benefit even without needing long-term care. Although premiums exceed stand-alone LTC insurance, many Americans find hybrid products create proper balance between potential long-term care needs and premium optimization.

What does Dave Ramsey say about hybrid LTC insurance?

Dave Ramsey recommends purchasing long-term care insurance to protect peace of mind and savings. He states Medicaid should never be a first choice for long-term care coverage. Regarding optimal purchase age, Dave suggests waiting until age 60 because the long-term care claim probability beforehand is quite slim.

Ready to Protect Your Future?

Get a personalized quote from a licensed specialist who can help you find the right hybrid long term care plan for your unique situation.